I am the founder and CEO of Argus Insights, a leader in Experience Analytics. Argus was started in stealth mode in 2008 to answer the question, "How can Market Research be improved and help drive innovation instead of validation?"I was the Executive Director of the ME310 Global Design Innovation Course at Stanford University. The course has a forty year history of developing tomorrow’s innovation leaders.Formerly I was the Chief Technologist for SK Telecom America’s R&D Group. In this role I was responsible for understanding how the rapidly changing technology landscape would enable SK Telecom to craft new business opportunities in the Americas. My areas of responsibility ranged from NGN wireless technologies (LTE vs WiMaxx, etc), handheld experiences & the interface technologies that enable them (multitouch touchscreens, haptic feedback, smartphone operating systems), as well as evolving influences on the telecommunications market (cloud computing, femtocells, CDN’s, LBS, SNS, etc.) I also supported SKTA’s internal Business Development & Corporate Venture Capital organizations.Prior to my role at SKTA, I led Synaptics efforts for developing next generation capabilities for handheld devices from within the marketing organization. I was responsible for developing a comprehensive competitive landscape for the various handheld markets, with specific focus on the mobile ecosystem, driving the product & technology strategy, in partnership with the engineering organization, to architect & execute our roadmap of future capabilities.I was also the architect of the Onyx Concept Phone, the world’s first multitouch mobile experience. I worked with the top handset manufacturers on the creation of tomorrow’s handsets, ensuring the right marriage of technology & user experience takes place as we see an industry transformation take place around multitouch technologies.

While Forbes had a pretty good article in on Kids Wearables back in March, they missed a huge opportunity in the kids wearable space. Impact tracking! You’re not worried about kids getting their 10,000 steps in when they can’t even walk yet. But you do worry about falls. If you’ve ever parented a little one, you know the drill. You hear a crash, a boom, something that makes your heart stop and you rush into the room where this cacophony of disaster originated. You are greeted with silence, a look, a pause, and then a wail. Because you don’t know whether this boom registered a 8.7 on the Richter scale, you don’t know whether to console or open up a can of “you’re okay, toughen up” love. Imagine if we could instrument toddlers with the same accuracy of crash test dummies! Is that a fake cry or did they really hit the floor at 50 mph? So imagine your child is wearing a onesie with more sensors than your average crash test dummy. You could immediately be alerted where they hit, how hard and if it hurts. That critical bit of evidence could be the difference between a calming mosey or a panic sprint to your child. Imagine the tears saved on both sides with this time saving concept in place!

Harvey has hit Houston and the surrounding areas very hard and that’s an understatement. Carriers have scrambled, to support the disaster, offering free calls and data to those impacted by the storm. Google Loon has been mentioned as one way to provide connectivity to impacted regions but balloons do not do as well in hurricane force winds. Imagine then a set of floatable base stations, leveraging either cellular or unlicensed wi-fi technologies, to provide on demand connectivity in the stricken region. These floats could be pre-installed in threat areas as well as the apps to make use of them. Additional floats could be dropped in by air after the winds die down to increase coverage or replace damaged nodes in the network. Power would only have to work for the first few days, when connectivity is so critical yet when those resources are most strained.

Thoughts? Imagine if we had automatically deployed floating wireless base stations to provide connectivity during that critical first 72 hours after a disaster…

A few years ago I was interviewed for a story on what were the barriers to adoption within the overall Smart Home market. One of the key that came out of the research I shared was the ongoing challenges that DIY consumers had with installation. Issues of WiFi range and configuration, device interoperability and just plain hardware quality kept consumers from having the joy of a more intelligent home within the first five minutes of opening the box.

First Half 2015 Consumer Perceptions of Smart Home Installation Experience by Category. Notice that how high the percentage of reviews mention a negative experience with installation.

Not only is there a lot of red in 2015, the percentage of green was a bit anemic as well. Consumers were really wrestling with Wi-Fi configuration, and other major stumbling blocks as they work through the agonies of installation. Cut forward to 2017 and there is an happier ending approaching, or better yet, happier beginning.

First Half 2017 Consumer Perceptions of Smart Home Installation Experience by Category

Looking at the same slice of consumer perceptions in the first half of 2017, we see less negative perceptions in some segments, growth in positive views across all segments. Suffice to say, the installation experience has improved within the Smart Home, correlating with a growth in the overall market as well.

Segment

% Reduction in Frustration

Smart Detectors

22.9%

Smart Doorbell Cameras

33.9%

Security Cameras

32.6%

Smart Lights

47.6%

Smart Sensors

12.2%

Smart Thermostats

15.1%

Smart Switches and Plugs

32.8%

As you can see in the table above, some of the most frustrating segments like Doorbell Cameras and Switches and Plugs saw significant improvements in their installation process for DIY consumers. These manufacturers worked hard to smooth out the kinks in their Out Of Box Experience and we see evidence of this in our consumer data.

Unfortunately, we are not out of the woods just yet. For the overall market, oddly, the frustration levels remained the same. So for each of these categories that have improved, there are categories where installation became more frustrating, including Smart Locks and Smart Home Hubs and Kits. Part of this, based on the market growth over the past few years, we are moving from the early adopters (many of which still have their X10 systems running) into the main part of the market. It is understandable that as a wider part of the target market embraces the promise of the Smart Home, more opportunities for frustration in installation can arise. The fact it is not substantial worse portends even more improvements in the future.

If you want to stay on top of consumer reaction to Smart Home, leverage the Argus Analyzer where we gather and analyzer all of the consumer review data across a broad array of devices and mobile applications. Like a focus group that never goes homes, subscribers can access the views of millions of consumers, getting early warning of the success and failure of products before the numbers come out and unpack the details as to why consumer sentiment is changing within the Smart Home market. Sign up for a free account today!

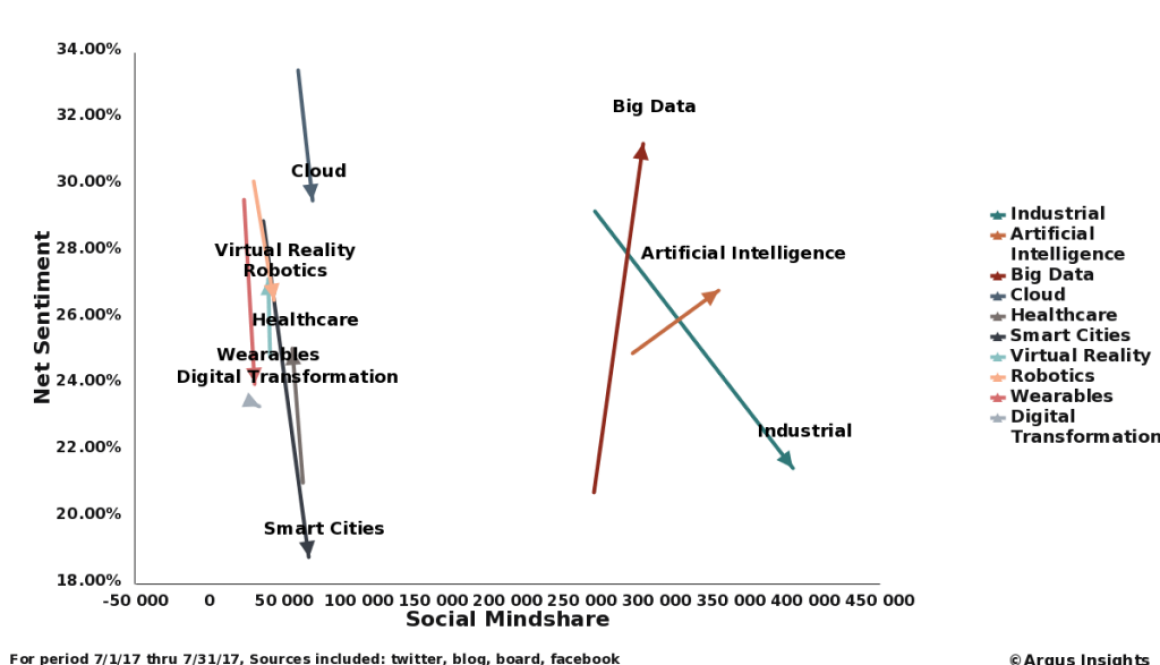

Looking back over the over one million Internet of Things tweets during the month of July, we routinely look to see which sub segments of IoT received the most mindshare. Though it rarely correlates to market share (Asset Tracking, one of the big early wins in IoT, receives very little mindshare) it is an early indicator of where the market is moving next. We published a similar analysis here and will continue this trend until the sun burns out of hydrogen or our readers tell us to stop.

Mindshare shifts in the Internet Of Things conversations between June and July 2017. Healthcare showed some impressive gains while Industrial IoT still leads within the segments.

Chatter about Industrial IoT moved past AI and Big Data for the first time in months, a clear indication that the hype (and actual deployments) around IIoT are increasing compared to June of 2017. AI and Big Data are often cobranded with IoT as they are seen as key solution elements in making sense and taking action on the projected petabytes coming from the billions of connected devices.

If you look at it, Industrial IoT is mentioned in about 40% of all IoT tweets, AI in around 30% and Big Data in about 25%. Everything else drops to Long Tail territory.

If you’re an IoT start-up, looking to get attention from experts and prospects alike, how are you making a dent within the storm of chatter happening in this market? When all of you advisors are coaching you to own a niche, how are you measuring the impact of your efforts? Sure, you slap #IoT on everyone one of your tweets announcing your launch, hoping Stacey or Junko might link back. But how do you move the needle in the data above? How do you raise the awareness of your category when all of your tools only help you push and measure your brand, in isolation?

That’s what we do at Argus Insights, providing tools and methods that give you an edge on understanding and influencing your category. We get all of the conversation, curate it using a mix of human and machine intelligence and serve it up so you can take action to move beyond the brand.

Looking back on the mindshare of the various applications of the Internet of Things within the IoT conversations on Twitter, we see a long tail forming, which is to be expected. This aligns with our Internets of Things view, that growth will come from a heterogenous set of architectures enabling enterprises large and small to benefit from the initial cost savings and eventual revenue growth from IoT powered solutions.

Long Tail of the Internet of Things shows the relative mindshare ranking of IoT application areas outside of the big areas of AI, Big Data, and Industrial IoT.

You can see from the graph above that since the beginning of June, Smart Cities, Cloud, HealthCare, VR, Robotics and Smart Home have lead the humps on the long tail of the Internet of Things. Surprisingly, application with some of the most actual market traction, Asset Tracking and Smart Grid, grab some of the smallest amount of mindshare within the IoT conversation. This supports the assertion that as IoT moves from concept to deployment, the conversation moves outside of IoT and into the area where the impact is being felt, further supporting the idea that branding of IoT as a solution is slowing market understanding and adoption, a concept we detailed here.

We are tracking the entire Internet of Things conversation. You can watch it unfold using the Argus Analyzer, our Real-Time IoT Ecosystem Intelligence tool!